Hot spot funds flow to thousands of stocks to evaluate stocks to diagnose the latest rating simulation transaction

Client

I. Overview of the strategy

The main contract of coking coal and coke futures was generally in a wide range of volatility in the first half of 2017. It once fell sharply and fell sharply after mid-year. The main reason was the improvement of fundamentals brought by supply-side reform and the expected increase in demand. Second, the funds are more concerned about the black sector, and the smaller coal char surface is relatively favorable for the market. From the analysis of the current fundamentals and disk performance, the coal coke futures sector should be more than empty. From the perspective of supply and demand, the beginning of the second half of the year, Jinjiu Yinshi is also the peak season for coal downstream demand. The arbitrage is considered from the fundamentals, and the strategy of multi-coke coke coal is recommended.

Figure 1: Schematic diagram of the recent trend of coke main contract J1709/J1801

Source: Huishang Futures Research Institute Wenhua Finance Wins Trading Software

From the trend point of view, the main trend of coke contract J1709 in the first half of this year is mainly a wide range of shocks, which in the May-June period, the sharp adjustment, the market confidence. Then, the coke 1709 contract was promoted by the relatively low supply of coke stocks of mainstream steel mills in the supply-side reforms and downturns. Together with the fuel boost, the company continued to rise for more than two months, and the growth rate was second to none in the commodity market. In the near future, it broke through the high point of 2016 and hit 2500 points.

Figure 2: Schematic diagram of the recent trend of coking coal main contract JM1709/JM1801

Source: Huishang Futures Research Institute Wenhua Finance Wins Trading Software

Compared with coke, coking coal is more moderate. As of the date of publication, although coking coal still maintains a unilateral bullish pattern, it has not yet broken through the 2016 high point, the slope is small, and the adjustment in the middle is greater than coke. The main reasons for coke being stronger than coking coal are as follows: 1. The supply elasticity of coke is poor, and the price is sensitive to the rotation change of inventory; 2. The role of coking coal in the reform of supply side is not as direct as that of coke; The frequent environmental inspections in the northern region and the administrative shutdown of coke have a greater impact; 4, the funds, especially the industrial funds, are more enthusiastic.

At present, the general trend of the commodity market is still warming up. In the process of the general increase in the market price of coking coal coke, there is no problem that the price is underestimated. At present, the focus of the market is mainly on the soaring varieties like this, and when it is crazy. . From the recent exchanges' adjustments to the black futures variety and the opening of the warehouse fee, the regulator's attitude toward controlling risk prevention can also be seen, but the temporary disk does not reflect a clear medium-term callback intention, so the current It is recommended to keep a long-term idea, and it is better to have a callback in the technical graphics.

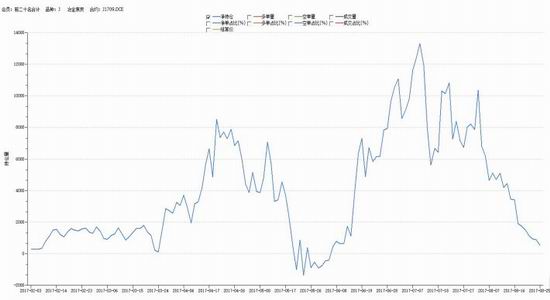

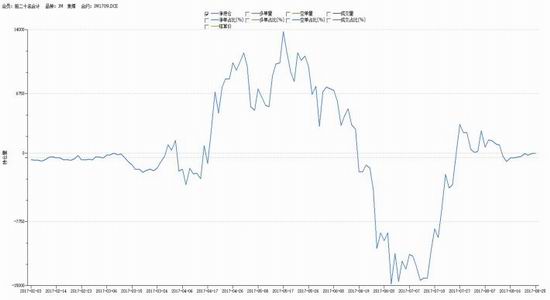

Figure 3: Schematic diagram of J1709 net long position

Figure 4: Schematic diagram of J1801 net long position

Source: Huishang Futures Institute Wind Information

Judging from the change in the main net position, after the J1709 continued to rise in the middle of the year, the net long position was obviously dominant, and the position was close to decline after the delivery month. At the same time, the main net long position of the main J1801 was extremely active, and formed upward. Obvious divergence pattern. In contrast to the relationship between long and short, the current position suggests that more than one support can still consider the intervention of the light warehouse, and the empty order should be extra cautious in the strong pattern.

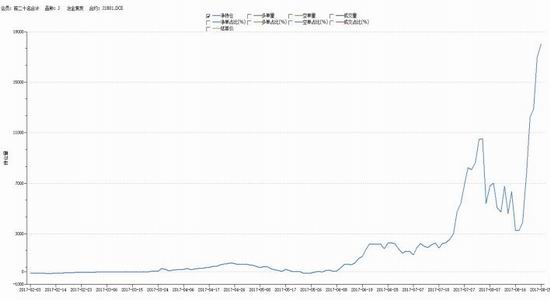

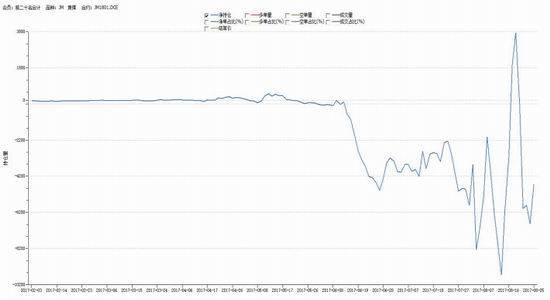

Figure 5: Schematic diagram of JM1709 net long position

Figure 6: Schematic diagram of JM1801 net long position

Source: Huishang Futures Institute Wind Information

Comparing the main contracts of coking coal JM1709 and JM1801, the trend of the disk reflects its own characteristics. First, the rate of increase is obviously less than that of coke. Second, the trading of distant contracts is relatively inactive. From the trend of JM1709, its volatility characteristics are close to the net long position, while the long-term contract has a large fluctuation in the main positions recently, which also reflects the uncertainty of the future disk trend.

Summary: In general, the black sector (including coal coke steel mines and other varieties) has maintained a relatively clear upward trend in recent days, and the bull market pattern is prominent, but the recent fluctuation frequency is relatively fast and the magnitude is large, which also brings a large operation. risks of. Coking coal coke varieties have similarities with glass, thermal coal and other varieties. The speculative attributes are heavier and the stability is poor. The main control panel and dishwashing are more significant on the disk surface. It is necessary to guard against the risk of short-term large fluctuations. It is recommended that the long-term contract on the far-month contract be the Lord. Strong coke contrast is recommended for multi-coke charcoal coal.

Second, macro and fundamental analysis:

1. The macro economy is basically stable, and there is no clear benefit to the variety of goods.

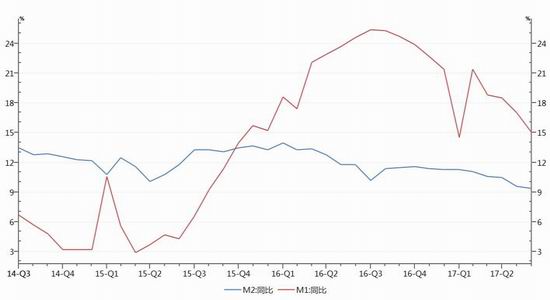

Figure 7: M1&M2 year-on-year diagram

Source: Huishang Futures Institute Wind Information

Figure 8: Schematic diagram of the main macroeconomic indicators

From the perspective of domestic macroeconomics, the current economic trend is basically stable, and some data have been adjusted at high points. GDP in the second quarter of the year still increased by 6.9%, which was significantly better than expected. At the same time, confidence in the overall commodity market was significantly boosted, but there were also concerns about the decline in growth in the second half of the year. In terms of monetary policy, the soaring M2 growth rate has seen a correction since the second half of last year. In the near term, the M1/M2 is in a downward trend, reflecting the trend of the central bank's contraction and de-leverage. It is expected that in the future, the macroeconomic situation and the impact of monetary policy on commodity markets will be considered neutral. The biggest factor for industrial products is undoubtedly the supply-side reform in the past two years. In 2017, the supply-side reform has entered a deepening year. As of June this year, the steel de-capacity task has been completed, and the coal-to-capacity task has been completed nearly 3/ 4. The industry pointed out that in the medium and long term, the Chinese economy is entering the second half of the transformation, and improving quality and efficiency is becoming the main tone of economic growth. Under this background, China's supply-side structural reform will continue to advance in depth, and it is expected that de-leverage will become the focus of the next supply-side structural reform.

The main macroeconomic indicators related to industrial products have been basically stable in the past six months. The recent growth rate of major economic indicators such as CPI, PPI and PMI has slowed down. Among them, the CPI growth rate in July was 1.40%, down 0.10% from the previous month and down 0.37% year-on-year. After the industrial PPI price index rebounded for 14 consecutive months, Recently, it fell slightly, and it was 5.5% in July, which was unchanged from the previous month and up 7.2% year-on-year. The manufacturing PMI index in July was 51.40, down 0.3% from the previous month and up 1.5% from the same period of last year, reflecting a certain degree of improvement compared with the same period of last year. The Caixin PMI index for the situation was reported at 51.10 in July, up 0.7% from the previous month and up 0.5% from the same period last year.

From the current point of view, the prices of industrial products continue to pick up. From the rise of the non-ferrous metal sector in the past two weeks, the rotation of the plate has begun, starting from black-colored-chemicals, but the current growth rate has Slowed down, some industrial products with higher gains (such as steel, coal char, iron ore, zinc, etc.) are facing a certain risk of callback at high levels. Therefore, in the current situation, they are still dominated by long-term ideas, but chasing more Must be cautious.

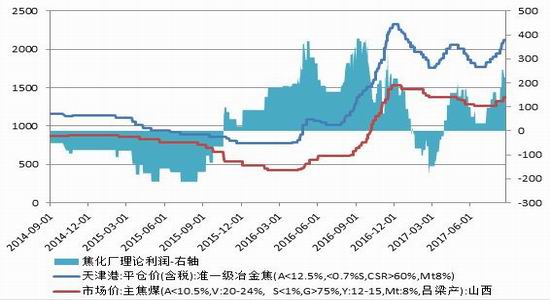

2. The fundamentals of the industry remain strong. 1) The price of coal coke is already at a high level in recent years.

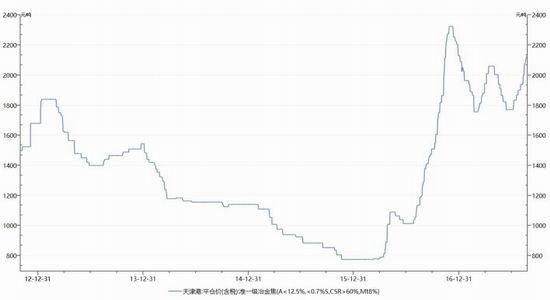

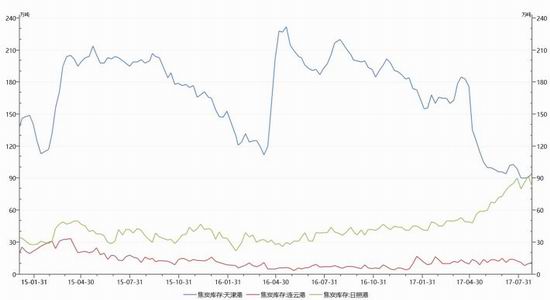

Figure 9: Schematic diagram of Tianjin Port's first-class metallurgical coke market price

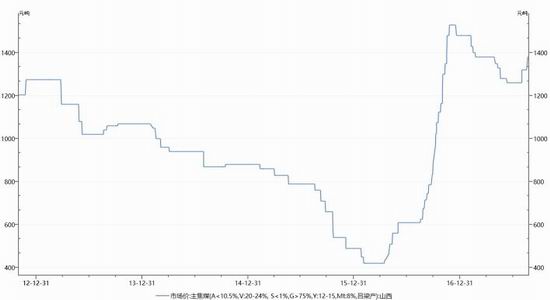

Figure 10: Schematic diagram of Shanxi coke coal market price

Source: Huishang Futures Institute Wind Information

From the price chart, it is already clear that since the end of 2015, the speed and magnitude of the rebound of coal coke prices is the highest in history. On the one hand, it is caused by the 7-8 year operation cycle of the macro economy. On the one hand, the supply-side reform promoted by the central government has played a positive role in boosting.

The role of supply-side reform in industrial products is focused on coal, steel, cement, etc. Among them, coking coal coke spans two key areas of coal and steel, which is undoubtedly the core variety of supply-side reform. From the current situation, coal market (including coking coal, coke, thermal coal and other varieties) is still good, especially in the traditional low season of coal consumption, demand is still tightening, on the one hand, downstream productivity is high under high profit stimulation. On the one hand, supply is subject to certain restrictions, and the quality of raw materials such as coal in the market is generally in short supply, and the price is firm.

2) The supply side is tight, and the stock supports the price.

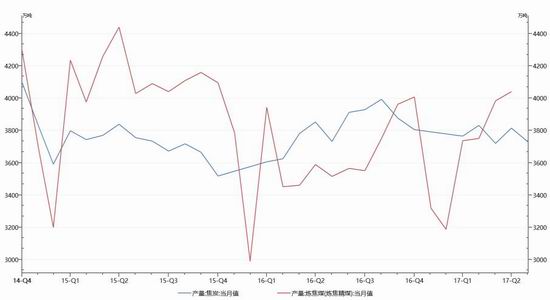

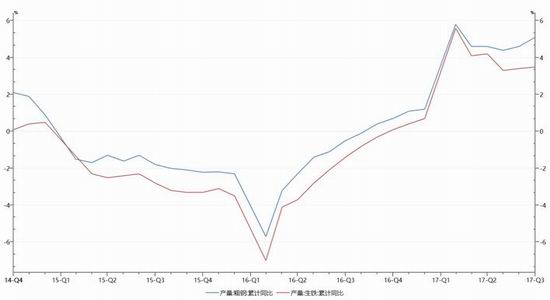

Figure 11: Schematic diagram of coking coal coke production (this month)

Source: Huishang Futures Institute Wind Information

Judging from the output of coke/coking coal, although supply-side reform is advancing, the year-on-year production has not been significantly reduced, but considering the decrease in coking coal imports and the recent steady growth of coke exports, domestic The current situation of tight supply of coal char has not changed substantially. In particular, with the concentration of replenishment of downstream enterprises in the second half of this year, it has obviously pushed up the price expectations of coke and iron ore, and the price of coking coal has formed a joint effect.

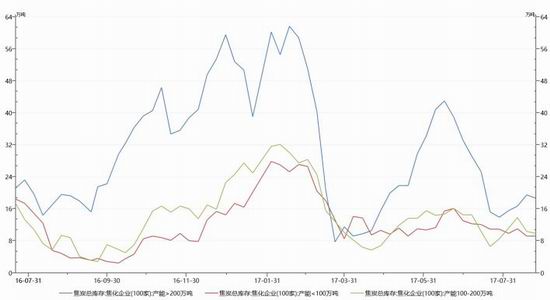

Figure 12: Schematic diagram of major port coke stocks

Figure 13: Schematic diagram of coke stocks in major coking enterprises

Source: Huishang Futures Institute Wind Information

Judging from the port inventory of coke and the inventory of major coking enterprises, the current inventory of coke is at a relatively low level, especially with the arrival of mainstream steel enterprises to replenish the inventory cycle, the main coke export port in the north - Tianjin Port The decline in coke stocks is significant. At the same time, although some coke stocks in some southern ports (such as Rizhao Port) have risen slightly, they cannot change the current situation of low coke inventory.

The inventory of finished products of major coking enterprises was also significantly lower than that of the same period of last year. In the traditional off-season demand, coke stocks have been at a low level, which has also aggravated the imbalance of coke supply end, and the price has been rising.

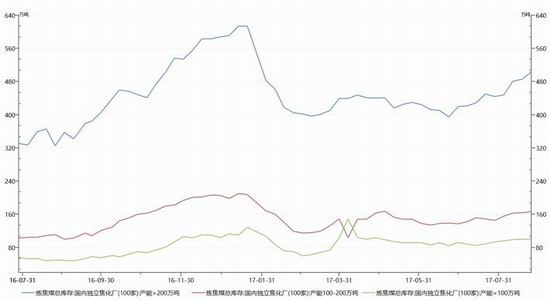

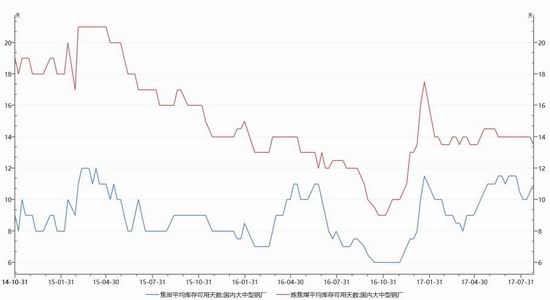

Figure 14: Schematic diagram of coking coal stocks in major ports

Figure 15: Schematic diagram of coking coal stocks in major coking enterprises

Source: Huishang Futures Institute Wind Information

The inventory of coking coal is similar to coke, but the difference in the terminal is that the inventory of coking enterprises is obviously showing signs of higher. This situation indicates that the upstream supply of coking coal (coal mine) is relatively loose, on the one hand, supply side reform and environmental protection. The measures are becoming more and more severe. The stimulation of the coking enterprises, for example, has occurred several times in the north (such as Tangshan area) from June to July. Due to environmental protection and holding meetings, the coking enterprises have been ordered to stop production due to administrative orders. This situation is also reflected in the market price, so we judge that in the current situation, the coke trend will be stronger than coking coal for a period of time.

Figure 16: Schematic diagram of the crude profit of the coking plant

Source: Huishang Futures Institute Wind Information

Judging from the crude profit of the coking plant, the current coking plant profit is still good. Although the coke price is high, the current production profit is not as good as the same period of last year due to the large increase in coking coal price. From the analysis of the annual operating conditions, the coking plant has basically got rid of the predicament. In addition to the first quarter of this year, the coking plant has a good production and operation. The main dilemma faced by the current coking plant is that there is still room for growth in coking coal prices, which will inevitably affect profits. The current basis is theoretically conducive to selling hedging, but coke prices (including futures prices) are soaring, it is difficult to choose a reasonable entry point. It is easy to generate huge floating losses on the disk.

3) The downstream demand for coal char is still stable and there are not many negative factors.

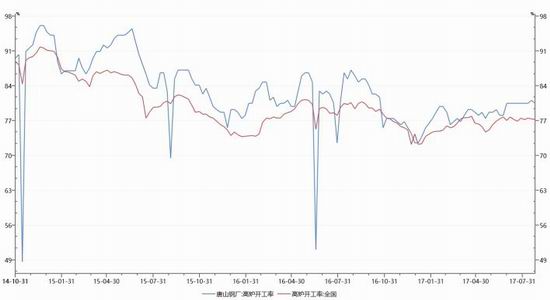

Figure 17: Cumulative year-on-year diagram of crude steel and pig iron production

Figure 18: Schematic diagram of the national/Tangshan blast furnace operating rate

Source: Huishang Futures Institute Wind Information

From the operating rate and output rate of downstream steel mills, the demand for coking coal coke is still quite strong. In the first seven months of this year, crude steel and pig iron production nationwide reached 5.1% and 3.5% year-on-year, up 5.6% and 4.9% respectively over the same period last year, and the growth rate exceeded the expected value. The output of coking coal and coke only increased slightly compared with last year, so the imbalance between supply and demand was gradually enlarged, resulting in the widespread shortage of market, which further pushed up the price of coking coal coke.

Figure 19: Schematic diagram of the days of coke/coking coal stocks in mainstream steel mills

Source: Huishang Futures Institute Wind Information

From the coking coal/coke inventory of mainstream steel mills, it is at a low level, and the iron ore replenishment stock is relatively active. The Huishang research is clear.

At the same time that the inventory days increased rapidly, the increase in the inventory days of coking coal coke was not obvious, and the supply of coal coke was also reflected from the side. It is expected that the supply and demand shortage of coal coke will not be alleviated before the steel mills begin to reduce the output rate at the end of the year. Signs.

Summary: The fundamentals of coking coal coke are generally more favorable. Due to the supply side reform and environmental protection policies, the supply is relatively tight, while the downstream demand is increasing, and the low inventory is conducive to pushing the price upward. Comprehensive analysis of coke coal coke prices in the second half of the year is expected to hit a new high, but the process may be tortuous with a large correction, I hope investors pay attention to risks, it is not recommended to chase high.

Third, the second half of the trend forecast and operational recommendations

According to the analysis of the current situation, it is expected that the coke coal and the future trend of the futures will remain stronger. The market is more clear, and the fundamentals are relatively stable and there is no large fluctuations. The attitude of the whole spot market is also optimistic. In this context, we expect the disk to be strong and with a narrow range of high shocks.

(1) Operational recommendations:

1. Short-term operation: It is recommended to have more trend or intraday operation. When multiple interventions are required, wait for the callback to be in place. The best timing is recommended when the callback is close to the Bollinger Middle Track and the KDJ and other graphic indicators are matched. Empty orders are not recommended for trending operations.

2, the mid-line operation: the trend of the mid-line is more, but considering the continuous rise in overdraft, the futures are more than the spot premium, the callback risk has increased, it is not recommended to do long-term orders.

3. Arbitrage: At present, due to the fundamental and disk trend, coke is stronger than coking coal, and the net long position is more active on coke 1801. It is recommended to do more coke to make arbitrage of coking coal. Proposal is based on the principle of reciprocity of funds in long and short positions.

(II) Specific operation strategy 1. Unilateral operation (coke): Operation type: J

Operation contract: J1801 operation direction: more

Admission range: Capital occupancy near 2230-2250 points: 30% operation lot: 80-90 lots

Stop loss range: 2150-2160 points target range: 2500-2550 points

2, unilateral operation (coking coal): operation variety: JM

Operation contract: JM1801 operation direction: more

Admission range: 1360-1380 points near the capital occupation: 30% of the operating lot: 200-250 hand stop loss range: 1320-1330 points target range: 1510-1550 points

3, arbitrage operation (multi-coking coal empty coke): operating varieties: J, JM

Operation contract: J1801, JM1801 Operation direction: Multi-J air JM entry price ratio: 1.20% of capital occupancy: less than 30%

Number of operations: J is about 45 hands, JM is about 125 hands. Stop loss range: Target range around 1.610: 1.680-1.690

Huishang Futures

Sina statement: Sina's posting of this article for the purpose of transmitting more information does not mean agreeing with its views or confirming its description. Article content is for reference only and does not constitute investment advice. Investors operate on this basis at their own risk.Enter [Sina Finance and Economics Unit] Discussion

Long Length Yoga Pants,Plus Size Long Pants,Extra Long Bootcut Jeans,Wide Leg Long Trousers

Ningbo Ysang Garment CO.,LTD , https://www.nilesone.com