Introduction: At 2 am Beijing time (June 16), the Federal Reserve will release the latest policy statement and economic and interest rate expectations. Due to the weak performance of the non-agricultural report in May and the uncertainties in the Brexit referendum, the market expects the Fed to keep interest rates unchanged at this week's meeting. Some investors have already expected the Fed to raise interest rates next time. Postponed until December.

Editor's Choice:

[Heavy event]>

Super Thursday comes to see how the four central banks affect the global market?

Britain's Brexit worries to suppress emerging Asian currencies and wait for the Fed's resolution to come out

[Ultimate Preview]

The Fed’s June policy meeting needs to focus on five key points

[Stock Market Impact]>

Super Thursday's attack on the Chinese stock market is less impact

The Fed’s current A-shares have been rejected and the Asian market is very anxious.

[risk prevention]>

Yin Yong, the central bank: the potential risk of effectively preventing and controlling the use of foreign exchange reserves

This week, the US and Japanese central banks will hold a meeting on interest rates, and next week the UK will hold a referendum on whether to stay in the EU.

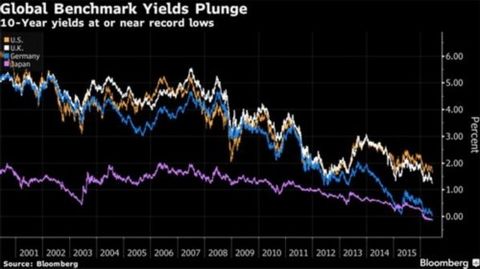

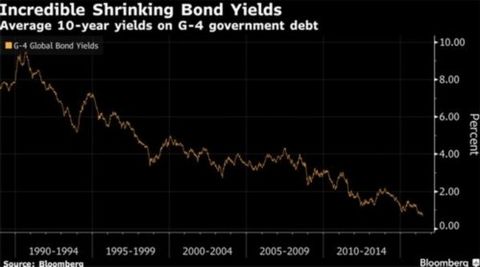

This week, the US and Japanese central banks will hold a meeting on interest rates. Next week, the UK will hold a referendum on whether to stay in the EU. Around these uncertainties (especially the Brexit referendum), the market has entered a comprehensive “safe haven modelâ€. Gold has risen for five days, and the yen is also approaching a new high since October 2014. Investors' demand for safe-haven assets seems to be unsatisfactory. Every day, you can see that some government bond yields have fallen to “zero.†Yesterday, the 10-year German bond yields fell below zero for the first time in record – It has once again set a milestone in the bond market.

The global economic growth is sluggish, negative interest rates are in the way, central banks vigorously buy bonds, making national debt very popular; even if the yield of more than 8 trillion US dollars bonds has fallen below zero, bond demand is still "not tired." Jack Malvey, the bond market, dates back to 1871 and can't find a period in which global bond yields are lower than they are today. Investors do not care about the price, the biggest worry is that demand is never ending, blind pursuit of exposing them to potential dangers, and may suffer terrible losses - especially when the Fed considers raising interest rates.

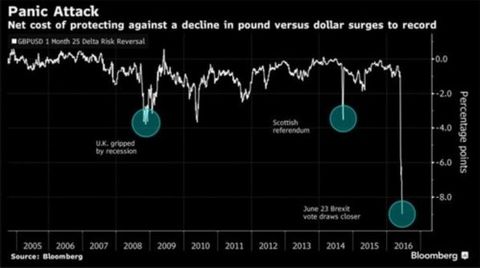

There is still a week away from the British "Brexit" referendum, and opinion polls increasingly show that the UK's departure from the EU may indeed become a reality. The pound has fallen to a two-month low against the dollar. The immediate response of investors is to increase the risk of hedging against the fall of the pound. The current put position in the 1980s is considered to have fallen to the level of the past three months. More than doubled.

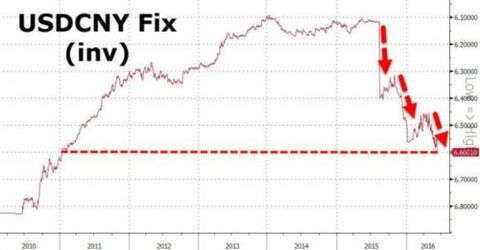

The other side, along with the slowdown in domestic economic growth and the risk of Brexit risk, the central bank today slashed the central parity of the yuan by more than 200 points, and for the first time since January 2011, the middle price was set at 6.60 yuan. The global market sell-off caused by the renminbi in August last year and January this year is still vivid, and this coincides with the Fed’s resolution announcement week. Can Queen Yellen live HOLD?

[Revenue is falling deeper every day! The demand for global government bonds seems to be “never endlessâ€

With risk aversion, we can basically get news of global bond yields falling to “zero†every day – from Asia, Europe, to the US. On Tuesday (June 14th), German government bonds ushered in a milestone, and the European benchmark 10-year German bond yields fell to negative values ​​for the first time. At this point, Germany, like Japan and Switzerland, the 10-year bond yield fell below zero. As the global economic outlook weakens and the polls show that the “Brexit†faction has gained more and more support before the British referendum, the decline in yields has accelerated.

The well-known financial blog Zerohedge wrote that the government bond yield will fall to what extent ? Every day the trend seems to tell us - "there is no end." Under the influence of global central bank asset purchases and the global gravity of the global economy, the actual situation may be: lower to the lower!

It is hard to imagine that the five-year bond yields of 11 countries in the world have fallen into negative values. Before getting the desired results (as the current situation, this target is inflation-oriented – but the data shows that inflation in developed economies fell 0.3% last year, the lowest since 2009), global central banks are always ready to continue to treasury bonds The rate of return is pushed lower.

"This is a crazy battle for defensive positions, and we are competing with global central banks," said Jack McIntyre, bond manager at Brandywine Global Investment Management.

Some people say that the QE policy, or the stimulus measures of the European and Japanese central banks' desperate efforts to purchase bonds, is the main reason for many bond markets to deviate from the fundamentals. This may help explain the US government's record high demand for government bonds this year. Almost all negative yield bonds are concentrated in the Eurozone and Japan, so investors invest their money in US Treasury bonds. After all, US bond yields are among the highest in industrialized countries.

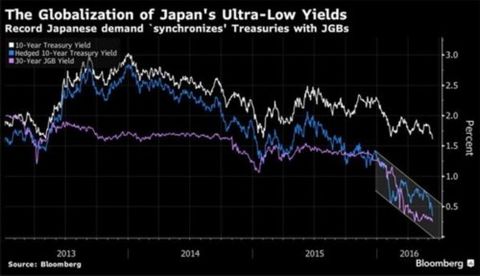

With the yen fund pouring into the US bond market at an unprecedented rate, Japan is delivering ultra-low bond yields to the world. On Wednesday (June 15), the yield of Japanese government bonds in various maturities hit a record low, and the 10-year bond yield fell to minus 0.18%.

Japan’s Ministry of Finance data showed that investors continued to buy US long-term Treasury bonds in April after Japanese investors bought about 5 trillion yen ($47 billion) in US dollar bonds in March. The cost of hedging against the yen's exchange rate risk has thus risen to the highest level since the global financial crisis.

Tohru Sasaki, head of Japanese market research at JPMorgan, expects Japanese and US debt to “converge†as Japanese investors compete for securities that bring the highest yields after hedging risks. Japanese life insurance companies and banks are basically working hard to combine the Japanese debt market with the US debt market. This is done by Japanese debt investors rather than foreign bond investors, so if the cost is higher, they are unlikely to lift the hedge. . This won't happen. For yen investors, the hedged US debt is actually equivalent to Japanese bonds, because Japanese bonds have no exchange rate risk.

In another case, investors are increasingly worried that the referendum on June 23 may lead to Britain leaving the EU. Analysts said the factor also boosted investor demand for sovereign bonds and spurred emerging Asian bonds. The rise in risk aversion in the past two weeks has boosted bond markets around the world, and Asia is expected to further loosen the potential capital gains that monetary policy will bring, as well as the relatively high yields in the region, which still makes it attractive.

A series of recent polls have shown that more British people are in favor of choosing to leave the EU next week's referendum. Some analysts believe that if the cause and effect of the Brexit, there will be more EU member states to follow suit (bond manager Gross said that if the British retreat may prompt France and Finland to follow suit). If these things happen, German 10-year bond yields may fall below minus 0.03%.

★ Vigilance: The global government bond market has been “forced into the cornerâ€!

Today's bond market is far from the known history. I am afraid I can't find a precedent that can be compared. Traders have left a lot of money, holding trillions of dollars in bonds, and the rate of return is pitiful. This situation has never been seen before. Investors do not hesitate to push up bond prices at all costs. The biggest worry is that demand is never ending, blindly pursuing them to expose them to potential dangers, and may suffer terrible losses – especially when the Fed considers raising interest rates.

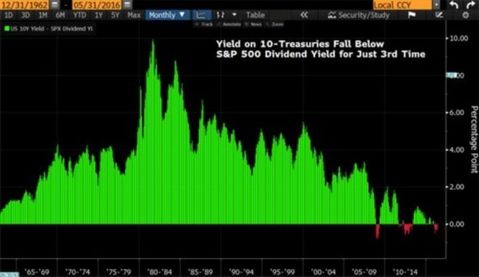

Torsten Slok, chief international economist at Deutsche Bank, said, "This will definitely make the market undetectable." In addition to the bond market bubble, history has its own veins. US 10-year Treasury yields are now lower than stock dividends – the third time in 50 years. The first two times, when the US debt hit this situation, it suffered a record annual decline.

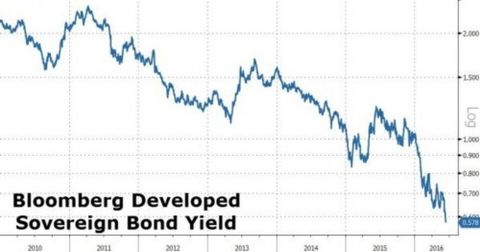

Bond risk is already high enough. According to data compiled by New York Mellon Bank, the average yield of 10-year Treasury bonds (over $25 trillion) in the United States, Japan, Germany, and the United Kingdom fell to 0.69% last week, a record low, and lower than the past 145 years. The average rate of return is 5%. With such low yields, bond investors do not have a bit of room to make mistakes.

The term premium for US 10-year Treasury bonds is now minus 0.47 percentage points. The term premium is supposed to be positive, mostly for the past 50 years. However, since the beginning of the year, the term premium has been converted into a discount, indicating that bond investors cannot withstand any risk of pushing up the rate of return. The same is true for Japan, Germany, and the United Kingdom; the term premiums have become negative as the benchmarks in these three markets have seen low innovations last week.

Stanley Sun, a New York strategist at Nomura Holdings, said, "The term premium should not be negative, but it is now the new normal."

[British Brexit really can become a reality! Investor risk hedging plus code]

The pound fell to a two-month low against the dollar yesterday, as a series of polls showed that more British people are in favor of choosing to leave the EU next week. The pound fell against 15 of the 16 major currencies, as five polls conducted by four companies showed that the Brexit camp was leading; in addition, the UK's best-selling newspaper, The Sun, supported the exit of the European Union on its front page.

The market's implied volatility hit a new high since March 2009 as the market worried that the Brexit camp would win the British referendum on June 23. The expected volatility index for the pound in the next two weeks rose to a record high of 40.5%, three times the level at the beginning of the month – the referendum on June 23 fell just during this period. In a speech on Wednesday (June 15), British Chancellor of the Exchequer George Osborne warned voters that if the referendum results in leaving the EU next week, he will take new measures, including tax increases and reductions.

There is still a week away from the British "Brexit" referendum, and opinion polls increasingly show that the UK's departure from the EU may indeed become a reality. Investors' response is to increase the risk of hedging against the pound's downside. This year, the bet on the pound's fall to 1.350 or lower after the June 23 referendum has reached 25 billion pounds.

If the pound really falls to 1.35, it will be more than 4% lower than the current exchange rate and fall below the 2009 low of 1.3503, returning to the level of September 1985. The cost of slamming the risk of falling pounds has now soared to a record high. In this situation, investors are still buying sterling put options, which fully shows that between time, they are no longer so firmly convinced that the UK is the biggest single in the world. The market is nonsense.

Alvin T. Tan, currency strategist at Société Générale in London, said, “Recently, we have seen all kinds of polls show that the 'Brexit' camp is full of momentum, which leads to a rebound in risk. This concern is even more on options. Obviously, the two-week sterling volatility is at an all-time high. If the polls continue to show the momentum of 'Brexit', the pound may explore the 1.3900 level on the eve of the vote."

“The pound sterling exchange and options market has been being led by the polls recently. It was almost two weeks ago that the market was still indifferent.†As early as the end of 2015, Societe Generale had already voted against the UK’s “Brexit†referendum. The potential risks raised warnings that most people expected the pound to strengthen.

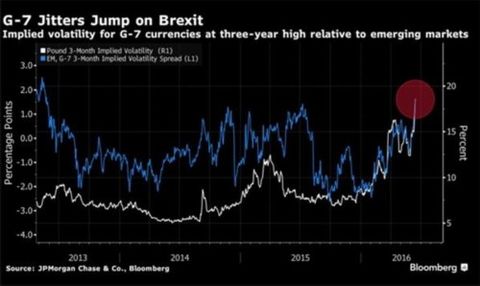

The market panicked - JP Morgan Chase's G7 currency volatility climbed to a three-year high against similar indicators in emerging market currencies. The three-month implied volatility of the G7 currency rose to 12.8% on Tuesday, surpassing the revaluation rate in emerging markets since May 2013.

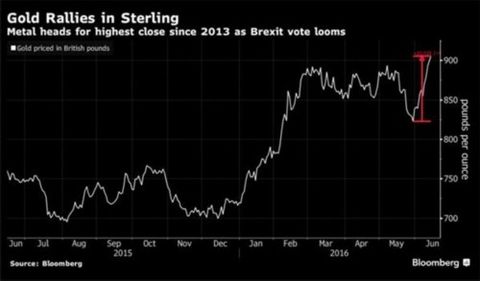

With the “Brexit†camp leading in the recent British polls, gold has led the way in asset varieties. Gold prices, priced in pounds, have climbed nearly 9% this month due to risk aversion and a fall in the pound, and touched £912.52 per ounce ($1287.47) on Tuesday (June 14), since August 2013. highest.

[The middle price fell below 6.60 for the first time in nearly five and a half years, and Yellen is facing difficulties again]

Zerohedge wrote that it seems to be a well-arranged script - in case the Fed unexpectedly raises interest rates tomorrow, it shocked the market. The Chinese central bank sent a signal to the market earlier this morning by devaluating the central parity of the yuan. will happen.

On Wednesday, the central parity of the RMB against the US dollar was reported at 6.6001 yuan, a sharp decrease of 210 points from the previous day, the lowest since January 12, 2011. Onshore renminbi fell 0.19% in yesterday's night trading, at 6.5966 yuan, the lowest since February 2011, and the previous month's decline expanded to 1%. Offshore renminbi expanded its decline by more than 100 points after MSCI “three refusals†of China A shares, setting a new four-month low.

Today, for the past 10 months, the People’s Bank of China has depreciated the central parity of the RMB for the third time. (Remember the "one-off depreciation" that China said when it depreciated the central parity in August last year?). Every time the central parity of the RMB has depreciated sharply, the US stocks will not find any benefits, not to mention the high valuations, and there is always a risk of a bubble burst.

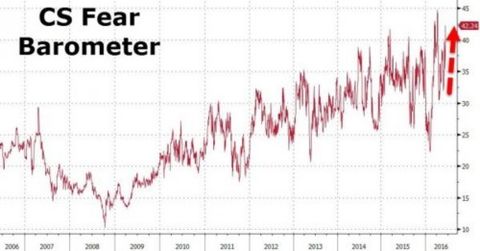

Jinhui Finance has already introduced it earlier. The CS Fear Barometer, which measures the confidence of the US stock market, has soared to a record high before the US Bank of Japan's resolution and the next week's risk event such as the Brexit referendum.

The Fed will announce the latest interest rate decision on Thursday (June 16) in Beijing time. The federal funds rate futures suggest that traders expect the Fed to raise interest rates in June, and the most recent meeting to raise interest rates by more than 50% will have to wait. February next year.

In the matter of the Fed’s rate hike, the decline in economic data – albeit perhaps just a sudden fluctuation in non-agricultural employment data – has made the rate hike in June become unreachable for the Fed, even in July.

However, it should be noted that even if the probability of raising interest rates is greatly reduced, the Fed maintains an essential optimism about the economic outlook. Yellen’s speech last week was particularly evident, when she warned against over-interpreting the employment data for May. Yellen’s ideas are quite in tune with the basic views of FOMC officials. Given that the Fed hopes to continue to raise interest rates slowly and reach inflation targets from below, the Fed expects to raise interest rates in the near future. This is why the interest rate hike is kept on the desktop.

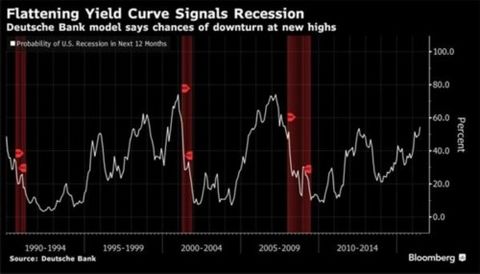

For now, however, the difference between the yields of 10-year US Treasury bonds and two-year Treasury bonds is the narrowest since 2007. A model of Deutsche Bank analyst Steven Zeng, which adjusted for short-term interest rates at historically low levels, suggests that the yield curve predicts a 55% probability of a recession in the US in the next 12 months. This is the highest probability of decay generated by this model since the current economic expansion period.

Coincidentally, JPMorgan Chase also pointed out that the probability of the US entering the recession next year is the highest since the beginning of this period of economic expansion. These have given Fed officials a reason to worry when they meet this week.

[The US-Japan Central Bank meeting kicked off: What should investors expect? 】

The Fed meeting kicked off, and some of the world's most influential central banks will also be busy for two days. The Fed and the Bank of Japan, the Bank of England and the Swiss National Bank are scheduled to announce monetary policy decisions this week. There is no doubt that the general expectation is that they will not move. If there is an accident in the decision-making, it is true and unexpected.

★ Federal Reserve

This is a round of predictions, and more attention needs to be paid to the policy statement issued by the FOMC. There are also economic expectations (1), the well-known interest rate expectations "bitmap" (2) and Chairman Yellen's press conference (3).

Participants may slightly cut their economic growth expectations to reflect the weak performance in the first quarter, but it depends on how much they increase their expectations for growth in the second quarter.

Yellen will choose the middle route between optimism and pessimism. Keeping the option to raise interest rates in July will be her main goal. Given that even Yellen has already believed that the economy is close to full employment, the Fed will not give up the position that the second quarter economic rebound will give it a reason to raise interest rates in July. After all, Yellen’s optimistic description tells us that the Fed is ready and willing to raise interest rates. However, policymakers have never been able to find consistent data as a reasonable justification for their interest rate hikes. The lack of strong data support has caused them to lose the opportunity to raise interest rates in June, and the hopes for July are not great. Therefore, investors have reason to look to September.

All in all, the Fed will not stand still this week. It can be expected that the FOMC policy statement will remain the same for inflation – the market-based inflation indicator is low and the survey-based inflation indicator is stable. A possible situation is that the University of Michigan's long-term inflation expectations fell to a record low of 2.3% in June, which may cause the Fed to abandon this assessment, but it will appear that the Fed is biased towards doves and may lead to a rate hike this year. Sex does not exist.

The Fed is not ready for this. It will be difficult for the FOMC to agree on a risk assessment. Fed Governor Lael Brainard will resist an assessment of the risk balance. This helps the Fed not to reveal the cards for July. "British Brexit" will make investors worry, but the Fed will not only focus on this issue. Strong retail data, job vacancies data and the number of initial jobless claims that were still low at Tuesday made the disappointing non-farm payrolls in May seem out of place.

If it were not for the United Kingdom to hold a referendum on EU membership on June 23, the possibility of a rate hike in June may be much higher. See if the FOMC statement is in talks with July or September, and what to say. Although the Fed statement may not mention "British Brexit", the upcoming referendum may become the first question Yellen was asked.

★ Bank of Japan

The renewed rise in the yen will make the Bank of Japan's policy-makers even more difficult to make interest rate assessments this week, but despite the signs of weakening inflation, many of them still seem to be inclined to temporarily expand the stimulus.

The shocking decision of President Haruhiko Kuroda to implement a negative interest rate policy earlier this year led to a stronger yen – not a weaker one. Policy makers were repeatedly criticized in the Japanese parliament and the media. However, if the yen continues to climb, then the ruling of Kuroda may once again unexpectedly relax the market, analysts said, but the Japanese staff is much higher than 105 yen against the dollar, this is all possible.

The British referendum is likely to make a choice to withdraw from the EU, which is the short-term biggest concern for Bank of Japan officials, but also provides reasons for their inability to stand before the June 23 referendum.

Standard Chartered analysts Betty Rui Wang and Mayank Mishra said the Bank of Japan may maintain its monetary policy this week, under the influence of Brexit risk and domestic factors. If the UK referendum results in a Brexit, resulting in market turmoil or prompting the Bank of Japan to further relax its policy, it may want to save ammunition to cope with this situation. The postponement of the increase in consumption tax and Prime Minister Shinzo Abe’s commitment to adopt bold fiscal stimulus measures this fall may also ease the pressure on the Bank of Japan to relax its policies.

However, if it is not the central bank that is most likely to take action this week, it is definitely not the Bank of Japan. However, the predictions of economists are not uniform. If there is any change in the meeting on Thursday, it may be the size and composition of the Bank of Japan’s asset purchases. In other words, expand quantitative easing. In addition, the Fed’s interest rate decision, one day earlier than the Bank of Japan, and the published policy statements may also affect the Bank of Japan’s resolution. (Jinhui Finance)

Editor's Choice:

[Heavy event]>

Super Thursday comes to see how the four central banks affect the global market?

Britain's Brexit worries to suppress emerging Asian currencies and wait for the Fed's resolution to come out

[Ultimate Preview]

The Fed’s June policy meeting needs to focus on five key points

[Stock Market Impact]>

Super Thursday's attack on the Chinese stock market is less impact

The Fed’s current A-shares have been rejected and the Asian market is very anxious.

[risk prevention]>

Yin Yong, the central bank: the potential risk of effectively preventing and controlling the use of foreign exchange reserves

This week, the US and Japanese central banks will hold a meeting on interest rates, and next week the UK will hold a referendum on whether to stay in the EU.

This week, the US and Japanese central banks will hold a meeting on interest rates. Next week, the UK will hold a referendum on whether to stay in the EU. Around these uncertainties (especially the Brexit referendum), the market has entered a comprehensive “safe haven modelâ€. Gold has risen for five days, and the yen is also approaching a new high since October 2014. Investors' demand for safe-haven assets seems to be unsatisfactory. Every day, you can see that some government bond yields have fallen to “zero.†Yesterday, the 10-year German bond yields fell below zero for the first time in record – It has once again set a milestone in the bond market.

The global economic growth is sluggish, negative interest rates are in the way, central banks vigorously buy bonds, making national debt very popular; even if the yield of more than 8 trillion US dollars bonds has fallen below zero, bond demand is still "not tired." Jack Malvey, the bond market, dates back to 1871 and can't find a period in which global bond yields are lower than they are today. Investors do not care about the price, the biggest worry is that demand is never ending, blind pursuit of exposing them to potential dangers, and may suffer terrible losses - especially when the Fed considers raising interest rates.

There is still a week away from the British "Brexit" referendum, and opinion polls increasingly show that the UK's departure from the EU may indeed become a reality. The pound has fallen to a two-month low against the dollar. The immediate response of investors is to increase the risk of hedging against the fall of the pound. The current put position in the 1980s is considered to have fallen to the level of the past three months. More than doubled.

The other side, along with the slowdown in domestic economic growth and the risk of Brexit risk, the central bank today slashed the central parity of the yuan by more than 200 points, and for the first time since January 2011, the middle price was set at 6.60 yuan. The global market sell-off caused by the renminbi in August last year and January this year is still vivid, and this coincides with the Fed’s resolution announcement week. Can Queen Yellen live HOLD?

[Revenue is falling deeper every day! The demand for global government bonds seems to be “never endlessâ€

With risk aversion, we can basically get news of global bond yields falling to “zero†every day – from Asia, Europe, to the US. On Tuesday (June 14th), German government bonds ushered in a milestone, and the European benchmark 10-year German bond yields fell to negative values ​​for the first time. At this point, Germany, like Japan and Switzerland, the 10-year bond yield fell below zero. As the global economic outlook weakens and the polls show that the “Brexit†faction has gained more and more support before the British referendum, the decline in yields has accelerated.

The well-known financial blog Zerohedge wrote that the government bond yield will fall to what extent ? Every day the trend seems to tell us - "there is no end." Under the influence of global central bank asset purchases and the global gravity of the global economy, the actual situation may be: lower to the lower!

It is hard to imagine that the five-year bond yields of 11 countries in the world have fallen into negative values. Before getting the desired results (as the current situation, this target is inflation-oriented – but the data shows that inflation in developed economies fell 0.3% last year, the lowest since 2009), global central banks are always ready to continue to treasury bonds The rate of return is pushed lower.

"This is a crazy battle for defensive positions, and we are competing with global central banks," said Jack McIntyre, bond manager at Brandywine Global Investment Management.

Some people say that the QE policy, or the stimulus measures of the European and Japanese central banks' desperate efforts to purchase bonds, is the main reason for many bond markets to deviate from the fundamentals. This may help explain the US government's record high demand for government bonds this year. Almost all negative yield bonds are concentrated in the Eurozone and Japan, so investors invest their money in US Treasury bonds. After all, US bond yields are among the highest in industrialized countries.

With the yen fund pouring into the US bond market at an unprecedented rate, Japan is delivering ultra-low bond yields to the world. On Wednesday (June 15), the yield of Japanese government bonds in various maturities hit a record low, and the 10-year bond yield fell to minus 0.18%.

Japan’s Ministry of Finance data showed that investors continued to buy US long-term Treasury bonds in April after Japanese investors bought about 5 trillion yen ($47 billion) in US dollar bonds in March. The cost of hedging against the yen's exchange rate risk has thus risen to the highest level since the global financial crisis.

Tohru Sasaki, head of Japanese market research at JPMorgan, expects Japanese and US debt to “converge†as Japanese investors compete for securities that bring the highest yields after hedging risks. Japanese life insurance companies and banks are basically working hard to combine the Japanese debt market with the US debt market. This is done by Japanese debt investors rather than foreign bond investors, so if the cost is higher, they are unlikely to lift the hedge. . This won't happen. For yen investors, the hedged US debt is actually equivalent to Japanese bonds, because Japanese bonds have no exchange rate risk.

In another case, investors are increasingly worried that the referendum on June 23 may lead to Britain leaving the EU. Analysts said the factor also boosted investor demand for sovereign bonds and spurred emerging Asian bonds. The rise in risk aversion in the past two weeks has boosted bond markets around the world, and Asia is expected to further loosen the potential capital gains that monetary policy will bring, as well as the relatively high yields in the region, which still makes it attractive.

A series of recent polls have shown that more British people are in favor of choosing to leave the EU next week's referendum. Some analysts believe that if the cause and effect of the Brexit, there will be more EU member states to follow suit (bond manager Gross said that if the British retreat may prompt France and Finland to follow suit). If these things happen, German 10-year bond yields may fall below minus 0.03%.

★ Vigilance: The global government bond market has been “forced into the cornerâ€!

Today's bond market is far from the known history. I am afraid I can't find a precedent that can be compared. Traders have left a lot of money, holding trillions of dollars in bonds, and the rate of return is pitiful. This situation has never been seen before. Investors do not hesitate to push up bond prices at all costs. The biggest worry is that demand is never ending, blindly pursuing them to expose them to potential dangers, and may suffer terrible losses – especially when the Fed considers raising interest rates.

Torsten Slok, chief international economist at Deutsche Bank, said, "This will definitely make the market undetectable." In addition to the bond market bubble, history has its own veins. US 10-year Treasury yields are now lower than stock dividends – the third time in 50 years. The first two times, when the US debt hit this situation, it suffered a record annual decline.

Bond risk is already high enough. According to data compiled by New York Mellon Bank, the average yield of 10-year Treasury bonds (over $25 trillion) in the United States, Japan, Germany, and the United Kingdom fell to 0.69% last week, a record low, and lower than the past 145 years. The average rate of return is 5%. With such low yields, bond investors do not have a bit of room to make mistakes.

The term premium for US 10-year Treasury bonds is now minus 0.47 percentage points. The term premium is supposed to be positive, mostly for the past 50 years. However, since the beginning of the year, the term premium has been converted into a discount, indicating that bond investors cannot withstand any risk of pushing up the rate of return. The same is true for Japan, Germany, and the United Kingdom; the term premiums have become negative as the benchmarks in these three markets have seen low innovations last week.

Stanley Sun, a New York strategist at Nomura Holdings, said, "The term premium should not be negative, but it is now the new normal."

[British Brexit really can become a reality! Investor risk hedging plus code]

The pound fell to a two-month low against the dollar yesterday, as a series of polls showed that more British people are in favor of choosing to leave the EU next week. The pound fell against 15 of the 16 major currencies, as five polls conducted by four companies showed that the Brexit camp was leading; in addition, the UK's best-selling newspaper, The Sun, supported the exit of the European Union on its front page.

The market's implied volatility hit a new high since March 2009 as the market worried that the Brexit camp would win the British referendum on June 23. The expected volatility index for the pound in the next two weeks rose to a record high of 40.5%, three times the level at the beginning of the month – the referendum on June 23 fell just during this period. In a speech on Wednesday (June 15), British Chancellor of the Exchequer George Osborne warned voters that if the referendum results in leaving the EU next week, he will take new measures, including tax increases and reductions.

There is still a week away from the British "Brexit" referendum, and opinion polls increasingly show that the UK's departure from the EU may indeed become a reality. Investors' response is to increase the risk of hedging against the pound's downside. This year, the bet on the pound's fall to 1.350 or lower after the June 23 referendum has reached 25 billion pounds.

If the pound really falls to 1.35, it will be more than 4% lower than the current exchange rate and fall below the 2009 low of 1.3503, returning to the level of September 1985. The cost of slamming the risk of falling pounds has now soared to a record high. In this situation, investors are still buying sterling put options, which fully shows that between time, they are no longer so firmly convinced that the UK is the biggest single in the world. The market is nonsense.

Alvin T. Tan, currency strategist at Société Générale in London, said, “Recently, we have seen all kinds of polls show that the 'Brexit' camp is full of momentum, which leads to a rebound in risk. This concern is even more on options. Obviously, the two-week sterling volatility is at an all-time high. If the polls continue to show the momentum of 'Brexit', the pound may explore the 1.3900 level on the eve of the vote."

“The pound sterling exchange and options market has been being led by the polls recently. It was almost two weeks ago that the market was still indifferent.†As early as the end of 2015, Societe Generale had already voted against the UK’s “Brexit†referendum. The potential risks raised warnings that most people expected the pound to strengthen.

The market panicked - JP Morgan Chase's G7 currency volatility climbed to a three-year high against similar indicators in emerging market currencies. The three-month implied volatility of the G7 currency rose to 12.8% on Tuesday, surpassing the revaluation rate in emerging markets since May 2013.

With the “Brexit†camp leading in the recent British polls, gold has led the way in asset varieties. Gold prices, priced in pounds, have climbed nearly 9% this month due to risk aversion and a fall in the pound, and touched £912.52 per ounce ($1287.47) on Tuesday (June 14), since August 2013. highest.

[The middle price fell below 6.60 for the first time in nearly five and a half years, and Yellen is facing difficulties again]

Zerohedge wrote that it seems to be a well-arranged script - in case the Fed unexpectedly raises interest rates tomorrow, it shocked the market. The Chinese central bank sent a signal to the market earlier this morning by devaluating the central parity of the yuan. will happen.

On Wednesday, the central parity of the RMB against the US dollar was reported at 6.6001 yuan, a sharp decrease of 210 points from the previous day, the lowest since January 12, 2011. Onshore renminbi fell 0.19% in yesterday's night trading, at 6.5966 yuan, the lowest since February 2011, and the previous month's decline expanded to 1%. Offshore renminbi expanded its decline by more than 100 points after MSCI “three refusals†of China A shares, setting a new four-month low.

Today, for the past 10 months, the People’s Bank of China has depreciated the central parity of the RMB for the third time. (Remember the "one-off depreciation" that China said when it depreciated the central parity in August last year?). Every time the central parity of the RMB has depreciated sharply, the US stocks will not find any benefits, not to mention the high valuations, and there is always a risk of a bubble burst.

Jinhui Finance has already introduced it earlier. The CS Fear Barometer, which measures the confidence of the US stock market, has soared to a record high before the US Bank of Japan's resolution and the next week's risk event such as the Brexit referendum.

The Fed will announce the latest interest rate decision on Thursday (June 16) in Beijing time. The federal funds rate futures suggest that traders expect the Fed to raise interest rates in June, and the most recent meeting to raise interest rates by more than 50% will have to wait. February next year.

In the matter of the Fed’s rate hike, the decline in economic data – albeit perhaps just a sudden fluctuation in non-agricultural employment data – has made the rate hike in June become unreachable for the Fed, even in July.

However, it should be noted that even if the probability of raising interest rates is greatly reduced, the Fed maintains an essential optimism about the economic outlook. Yellen’s speech last week was particularly evident, when she warned against over-interpreting the employment data for May. Yellen’s ideas are quite in tune with the basic views of FOMC officials. Given that the Fed hopes to continue to raise interest rates slowly and reach inflation targets from below, the Fed expects to raise interest rates in the near future. This is why the interest rate hike is kept on the desktop.

For now, however, the difference between the yields of 10-year US Treasury bonds and two-year Treasury bonds is the narrowest since 2007. A model of Deutsche Bank analyst Steven Zeng, which adjusted for short-term interest rates at historically low levels, suggests that the yield curve predicts a 55% probability of a recession in the US in the next 12 months. This is the highest probability of decay generated by this model since the current economic expansion period.

Coincidentally, JPMorgan Chase also pointed out that the probability of the US entering the recession next year is the highest since the beginning of this period of economic expansion. These have given Fed officials a reason to worry when they meet this week.

[The US-Japan Central Bank meeting kicked off: What should investors expect? 】

The Fed meeting kicked off, and some of the world's most influential central banks will also be busy for two days. The Fed and the Bank of Japan, the Bank of England and the Swiss National Bank are scheduled to announce monetary policy decisions this week. There is no doubt that the general expectation is that they will not move. If there is an accident in the decision-making, it is true and unexpected.

★ Federal Reserve

This is a round of predictions, and more attention needs to be paid to the policy statement issued by the FOMC. There are also economic expectations (1), the well-known interest rate expectations "bitmap" (2) and Chairman Yellen's press conference (3).

Participants may slightly cut their economic growth expectations to reflect the weak performance in the first quarter, but it depends on how much they increase their expectations for growth in the second quarter.

Yellen will choose the middle route between optimism and pessimism. Keeping the option to raise interest rates in July will be her main goal. Given that even Yellen has already believed that the economy is close to full employment, the Fed will not give up the position that the second quarter economic rebound will give it a reason to raise interest rates in July. After all, Yellen’s optimistic description tells us that the Fed is ready and willing to raise interest rates. However, policymakers have never been able to find consistent data as a reasonable justification for their interest rate hikes. The lack of strong data support has caused them to lose the opportunity to raise interest rates in June, and the hopes for July are not great. Therefore, investors have reason to look to September.

All in all, the Fed will not stand still this week. It can be expected that the FOMC policy statement will remain the same for inflation – the market-based inflation indicator is low and the survey-based inflation indicator is stable. A possible situation is that the University of Michigan's long-term inflation expectations fell to a record low of 2.3% in June, which may cause the Fed to abandon this assessment, but it will appear that the Fed is biased towards doves and may lead to a rate hike this year. Sex does not exist.

The Fed is not ready for this. It will be difficult for the FOMC to agree on a risk assessment. Fed Governor Lael Brainard will resist an assessment of the risk balance. This helps the Fed not to reveal the cards for July. "British Brexit" will make investors worry, but the Fed will not only focus on this issue. Strong retail data, job vacancies data and the number of initial jobless claims that were still low at Tuesday made the disappointing non-farm payrolls in May seem out of place.

If it were not for the United Kingdom to hold a referendum on EU membership on June 23, the possibility of a rate hike in June may be much higher. See if the FOMC statement is in talks with July or September, and what to say. Although the Fed statement may not mention "British Brexit", the upcoming referendum may become the first question Yellen was asked.

★ Bank of Japan

The renewed rise in the yen will make the Bank of Japan's policy-makers even more difficult to make interest rate assessments this week, but despite the signs of weakening inflation, many of them still seem to be inclined to temporarily expand the stimulus.

The shocking decision of President Haruhiko Kuroda to implement a negative interest rate policy earlier this year led to a stronger yen – not a weaker one. Policy makers were repeatedly criticized in the Japanese parliament and the media. However, if the yen continues to climb, then the ruling of Kuroda may once again unexpectedly relax the market, analysts said, but the Japanese staff is much higher than 105 yen against the dollar, this is all possible.

The British referendum is likely to make a choice to withdraw from the EU, which is the short-term biggest concern for Bank of Japan officials, but also provides reasons for their inability to stand before the June 23 referendum.

Standard Chartered analysts Betty Rui Wang and Mayank Mishra said the Bank of Japan may maintain its monetary policy this week, under the influence of Brexit risk and domestic factors. If the UK referendum results in a Brexit, resulting in market turmoil or prompting the Bank of Japan to further relax its policy, it may want to save ammunition to cope with this situation. The postponement of the increase in consumption tax and Prime Minister Shinzo Abe’s commitment to adopt bold fiscal stimulus measures this fall may also ease the pressure on the Bank of Japan to relax its policies.

However, if it is not the central bank that is most likely to take action this week, it is definitely not the Bank of Japan. However, the predictions of economists are not uniform. If there is any change in the meeting on Thursday, it may be the size and composition of the Bank of Japan’s asset purchases. In other words, expand quantitative easing. In addition, the Fed’s interest rate decision, one day earlier than the Bank of Japan, and the published policy statements may also affect the Bank of Japan’s resolution. (Jinhui Finance)

Toddler Girl Sandal,,White Canvas Trainers,Ladies Canvas Shoes,Canvas Boat Shoes

FOSHAN SHUNDE JIANGCHENG SHOES CO.,LTD , https://www.pulangdeshoe.com