This article was first published on the WeChat public account: the US period study. The content of the article belongs to the author's personal opinion and does not represent the position of Hexun.com. Investors should act accordingly, at their own risk.

Core point of view:

Last week, all sectors except banks and non-banking finances recorded gains. The mining and food and beverage industry led the gains. After the Belt and Road Summit, steel mills resumed production and production was strong; crude oil was affected by the extension of the production reduction agreement; the rise in US political risk caused a resurgence of risk aversion, and the dollar hit its biggest one-week decline in a year. Under the comprehensive factors, the price of industrial products in the mid-term industry has rebounded. However, the downstream consumption boom is generally the same, agricultural products 000061, the stock price continues to decline overall; the land market and commercial housing market continue to cool; only air conditioners in home appliances continue to maintain the previous growth rate. Under the situation that the overall downstream demand is weak, the current price increase of industrial products is unsustainable.

Upstream raw materials:

Saudi Arabia and Russia reached an agreement on the extension of the crude oil production reduction agreement, and the bullish oil price soared. Downstream consumption of base metals weakened, supply differentiation led to differentiation, and aluminum was expected to increase due to supply-side reform expectations. The rise in US political risk led to a sharp rise in risk aversion, and the VIX index rose 15.77%. Coal and iron ore rebounded sharply.

Midstream materials, manufacturing and delivery:

Steel led the black series to rebound strongly. Thread stocks fell rapidly, spot premiums and capacity expectations were strong, and the thread 1710 contract rose 10.3% this week. The cement glass fluctuated slightly, and the cement price increase was concentrated in North China, Northeast China and East China. From January to April, the cumulative output of excavators increased by 73.5% year-on-year, maintaining a relatively high growth rate. The cumulative production of heavy trucks in January-April increased by 10.44% year-on-year, and the cumulative sales growth rate was 10.44%. The production and sales rebounded for 16 consecutive months. In April, road freight decreased slightly to 9.28% year-on-year, and water transport rebounded to 8.7%. The container throughput of major ports nationwide maintained 7.7% year-on-year. The BDI index fell 5.72% to below 1,000 this week. Chemicals rebounded from crude oil.

Downstream optional consumption:

Real estate: land and commercial housing transactions fell. In the week of May 14th, the transaction volume of commercial housing in 30 large and medium-sized cities was 3,753,400 square meters, up 1.62% from the previous month and down 32.94% year-on-year. In the week of May 14, the supply area of ​​100 large and medium-sized cities was 9,803,900 square meters, up 22.4% from the previous month and down 5.14% year-on-year. The area of ​​land sold was 5,703,900 square meters, down 11.33% from the previous month and down 32.28 from the same period last year. The growth rate of home appliance output was different. From January to April, the growth rate of air conditioner production rose to 17.6% year-on-year. The growth rate of refrigerator production dropped to 12.4%, the washing machine dropped to 4.8%, and the growth rate of color TV continued to turn negative 7.9%.

Downstream consumption:

The overall price of agricultural products fell, and the prices of eggs and vegetables continued to fall. The overall downstream consumption boom is average.

Currency Exchange Rate:

The central parity of the renminbi against the US dollar ended six consecutive liters, ridding 174 basis points, the largest devaluation since February 20. The US dollar index fell 2.1% this week, the biggest weekly decline in a year.

|

![[Weekly] The overall downstream demand is weak, and the upstream price increase is difficult to sustain.](http://i.bosscdn.com/blog/bc/38/e0/249b2ffc28415c1460eb513ec9.jpg)

table of Contents

First, the upstream raw materials... 1

1.1 Crude oil natural gas: crude oil rebound... 2

1.2 Basic metal differentiation; precious metals go high... 2

1.3 Coal and iron ore: a sharp rebound... 3

Second, the middle reaches of the material... 4

2.1 Steel: Inventory decline... 4

2.2 Cement and glass: price shocks... 5

Third, the midstream manufacturing and delivery... 5

3.1 Excavator, heavy truck: production and sales continue to be strong... 5

3.2 Transportation and freight: The BDI index fell below 1000... 6

3.3 Chemicals: a sharp rebound... 7

Fourth, downstream optional consumption... 7

4.1 Real estate: land and commercial housing transactions double decline... 7

4.2 Automobiles: Production and sales in April decreased significantly year-on-year, passenger cars performed worse than commercial vehicles... 8

4.3 Home appliance output growth and differentiation... 9

V. Downstream consumption (9)

5.1 Agricultural products: the price of eggs and vegetables plummeted... 9

5.2 Others: Downstream Prosperity General... 10

6. Currency exchange rate: This week, the US dollar index hit the biggest one-week drop in a year... 11

First, upstream raw materials

1.1 Crude oil natural gas: crude oil rebound

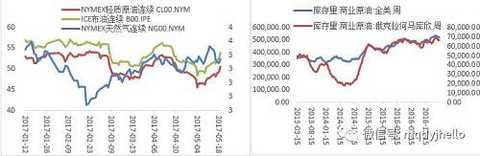

Saudi Arabia and Russia reached an agreement on the extension of the crude oil production reduction agreement, and the bullish oil price soared. NYMEX light crude oil rose 5.67% to US$50.53/barrel; oil week rose 5.68% to US$53.8/barrel; natural gas weekly rose-5.25% to US$3.246/million British thermal unit.

|

1.2 Basic metal differentiation; precious metals go higher

The downstream consumption of basic metals has weakened, and the supply of expected differentiation has led to a trend of differentiation. LME three-month copper week rose 0.27% to 5687.5 US dollars / ton; 3 months aluminum week rose 2.01% to 1943 US dollars / ton; 3 months zinc week rose -0.37%, to 2636 US dollars / ton.

The rise in US political risk led to a sharp rise in risk aversion, and the VIX index rose 15.77%. Comex gold week rose 2.3% to 1248.1 US dollars / ounce; silver week rose 2.51% to 16.775 US dollars / ounce.

1.3 Coal and iron ore: a sharp rebound

As of May 19, the average daily coal consumption of the six major power generations this month was 623,000 tons, which was flat compared with last week and was lower than the 638,000 tons in April. Ore main force 09 rose 8.6%, hot coil 1710 rose 9.8%; this week coking coal 09 rose 3.5%, coke 09 rose 4.3%, Zheng coal 09 rose 4.7%.

Second, the middle material

2.1 Steel: Inventory decline

This week's black series rebounded. Although there are a lot of bad information such as real estate regulation, steel mills have high profits, and consumption may turn weak, but the current thread inventory has dropped rapidly, the spot has risen and the capacity is expected to be strong. The thread has led a black rebound this week. The 1710 thread contract rose 10.3% this week.

2.2 Cement and glass: price shocks

The cement price index rose by 0.35% to 110.48, and the glass price index rose by 0.31% to 1091.19. The price increase area is concentrated in North China, Northeast China and East China.

Third, the midstream manufacturing and delivery

3.1 Excavator, heavy truck: production and sales continue to flourish

From January to April, the cumulative output of excavators increased by 73.5% year-on-year, maintaining a relatively high growth rate. The cumulative production of heavy trucks in January-April increased by 10.44% year-on-year, and the cumulative sales growth rate was 10.44%. The production and sales rebounded for 16 consecutive months.

3.2 Transportation and freight: BDI index fell below 1000

In April, road freight decreased slightly to 9.28% year-on-year, and water transport rebounded to 8.7%. The container throughput of major ports nationwide maintained 7.7% year-on-year.

In early May, China's highway logistics freight index continued to decline by 0.22% to 1067.47.

The BDI index fell 5.72% to 956.

|

3.3 Chemicals: a sharp rebound

Chemicals rebounded from crude oil. Among the main contracts, methanol rose 8.8%, PVC rose 8.5%, PP rose 8.2%, plastics rose 6.1%, asphalt rose 5.6%, PTA rose 3.1%, and Hujiao rose 1.8%.

Fourth, downstream optional consumption

4.1 Real estate: land and commercial housing transactions fell

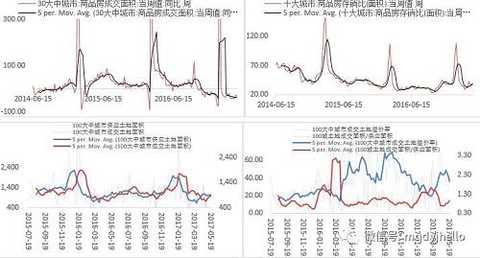

In the week of May 14th, the transaction volume of commercial housing in 30 large and medium-sized cities was 3,753,400 square meters, up 1.62% from the previous month and down 32.94% year-on-year.

In the week of May 14, the supply area of ​​100 large and medium-sized cities was 9,803,900 square meters, up 22.4% from the previous month and down 5.14% year-on-year. The area of ​​land sold was 5,703,900 square meters, down 11.33% from the previous month and down 32.28 from the same period last year.

|

4.2 Automobiles: Production and sales in April dropped significantly year-on-year, and passenger cars performed worse than commercial vehicles.

In April, the production and sales of automobiles decreased significantly from the previous month, and ended the year-on-year growth, showing a slight decline. Among them, the production of 2,138,400 units, down 17.88% from the previous month, down 1.91% year-on-year; sales of 2.084 million units, down 18.05% from the previous month, down 2.24% year-on-year. The production and sales volume of new energy vehicles were 37,306 and 34,361, respectively, up 19% and 7.9% respectively.

From January to April, the growth rate of automobile production and sales was slightly slower than that in the first quarter, and commercial vehicles still maintained rapid growth year-on-year. The production and sales of automobiles reached 9.725 million and 90.86 million, an increase of 5.38% and 4.58% year-on-year. The growth rate was 2.61 percentage points and 2.44 percentage points lower than that in the first quarter. Among them, the production and sales of passenger cars were 7,890,200 and 7,669,800, an increase of 4.18% and 2.47%; the production and sales of commercial vehicles was 1,381,300 and 1,146,200, an increase of 12.79% and 17.72%. From January to April, new energy vehicles produced 95,856 vehicles, with sales of 90,402 vehicles, an increase of 1.4% and a decrease of 0.2% over the same period of the previous year.

4.3 Home appliance output growth and differentiation

In the first seven months of January-April, the growth rate of air-conditioner production rose to 17.6% year-on-year, the growth rate of refrigerator production dropped to 12.4%, the washing machine dropped to 4.8%, and the growth rate of color TVs continued to turn negative by 7.9%.

V. Downstream consumption

5.1 Agricultural products: the price of eggs and vegetables plummeted

The price of pork rose by -1.19% to 20.83 yuan/kg in 28 weeks; the price of 28 key monitoring vegetables rose by -3.23% to 3.3 yuan/kg; the price of 7 key monitoring fruits was up and down in the week- 0.83% to 5.97 yuan / kg.

The price of bulk eggs rose by -4.95% to 4.22 yuan/kg. The price of large white chickens rose by -1.85% to 10.6 yuan/kg.

|

5.2 Others: Downstream generality

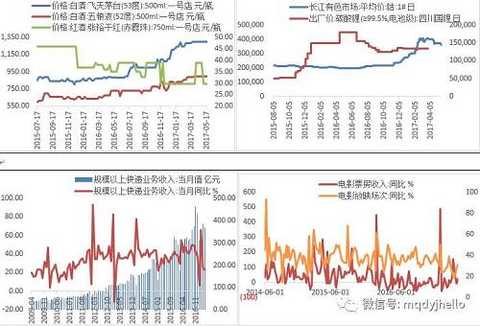

In the week of May 19, No. 1 shop Feitian Maotai 600519, stocks 53 degrees stable at 1299 yuan / bottle, Wuliangye 000858, shares 52 degrees stable at 899 yuan / bottle.

In the week of May 14th, the film market cooled down, with a box office receipt of 76 million yuan; 23.5 million people watching the movie; and 1.597 million screenings, which were less than the same period last month, but both year-on-year.

During the week of May 19, the price of cobalt fell to 357,500 yuan / ton.

The prosperity of the textile industry has stabilized, and the Keqiao Textile Price Index is 105.50.

On the morning of May 14, the Hainan tourism consumer price index fell back to 92.27.

In April, the revenue from express delivery above designated size was 36.93 billion yuan, an increase of 22.7% over the same period of the previous year, and the growth rate was lower than the same period of the previous year.

|

6. Currency exchange rate: This week, the US dollar index hit the biggest one-week decline in a year.

The onshore RMB against the US dollar closed at 16:30, at 6.8927, down 24 basis points from the previous trading day. The central parity of the RMB against the US dollar ended six consecutive gains, ridding 174 basis points, the largest adjustment since February 20, reported 6.8786. The US dollar index fell 0.78% to 97.1115. Earlier reports said that a White House official was a stakeholder in Trang’s ordinary Russian investigation. The US dollar index fell 2.1% this week, the biggest weekly decline in a year.

Cashmere Wool Scarf,Wool Cashmere Wrap,Cashmere Wool Wrap Scarf,Wool Cashmere Blanket Scarf

INNER MONGOLIA CASHMERE PRODUCTS CO., LTD. , https://www.grpashmina.com